Fintech is altering monetary providers for the higher. That’s the mantra. Or at the very least, it’s imagined to… That’s what everyone was and remains to be anticipating. The fintech wave, that nice innovation motion that notably occurred after the monetary disaster of 2008 is constructed on many guarantees. Certainly one of its strongest guarantees, although, is that it’s going to construct a extra inclusive monetary providers business. Notably by together with many extra girls than earlier than. And but, plainly it isn’t in any respect perfect- Removed from it. Notably in the case of gender stability and equality. Let’s dive in, what’s the state of girls in fintech right this moment?

“To ensure that shoppers to get the services and products that they want, we’d like not solely to begin investing in numerous concepts and founders but in addition be sure that the individuals across the desk making the funding choices are numerous. Right this moment, solely 2% of enterprise capital funding goes in direction of women-founded companies, and even lower than that goes towards girls of color. As an ecosystem, we should work collectively to create larger entry to alternatives and capital for feminine founders to assist drive innovation, new services and products, and an equitable future for all entrepreneurs.”

— Michelle Beyo, CEO of Finovator

“Even if you’re optimistic, it’s arduous to be content material in regards to the state of girls in fintech right this moment. There’s nonetheless a lot to do earlier than we’ve a very inclusive business. Fintech is failing its promise to be higher than good outdated monetary providers. Nonetheless, there are many causes to hope for a brighter future, if we proceed to push everyone in the correct route.”

— Tristan Pelloux, Chief Pencil Officer of Fintech Overview

The way it seems like in Europe, North America and elsewhere…

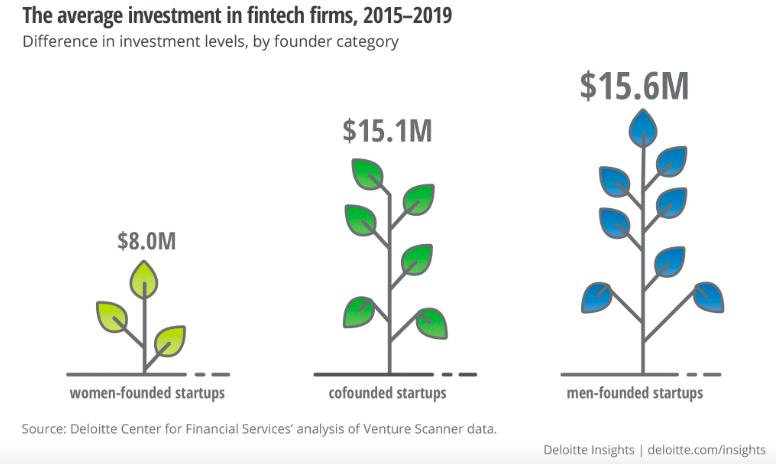

It’s clearly not the identical in the entire geographies. In some locations, it’s barely higher than others. That’s the excellent news, let’s say. The dangerous information is that globally, let’s not sugarcoat it, it isn’t nice in any respect. Let’s have a quick take a look at it from a numbers’ perspective: just one.5% of worldwide fintech corporations are based solely by girls. These corporations obtain simply over 1% of whole fintech funding based on Findexable. There are usually not 1,000,000 methods to take a look at these numbers and assume that we’re in a passable state.

Ladies are beginning much less fintech corporations, and getting even much less total funding after they finally do. Final however not least, girls are on common getting much less funding per funding spherical than men-founded startups. It’s a man’s man’s world in fintech, it appears. Very very similar to the outdated banking system that it’s disrupting.

Moreover, it’s fairly skinny when it comes to girls within the govt administration of fintech corporations. The biggest proportion of girls executives (26%) within the sector are Chief Individuals Officer or Head of HR. That’s adopted by Chief Advertising Officer (CMO) and Chief Monetary Officer (CFO). And of all fintech CEOs globally, 5.6% are girls, and fewer than 4% of girls maintain the title of Chief Innovation (CIO) or Expertise Officer (CTO).

Climbing the pyramid…

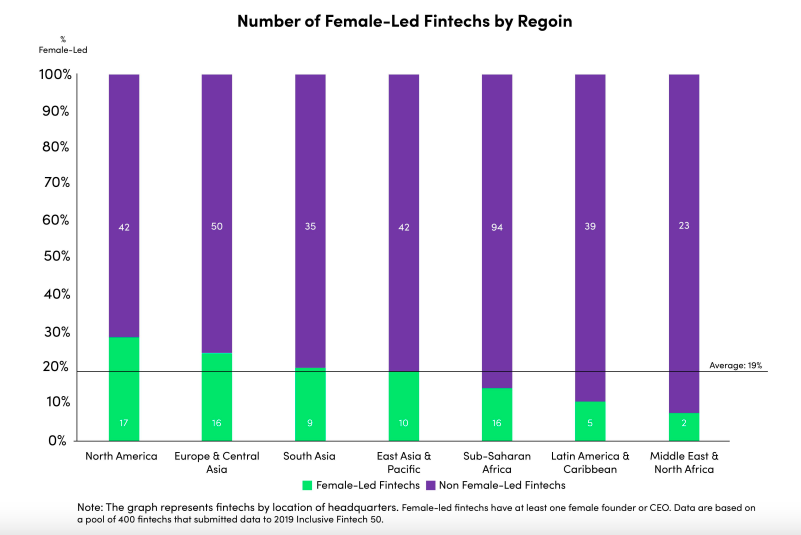

In North America, solely 4.8% of firm founders are girls, in comparison with 7.7% of girls founders in Asia, 7.4% in Africa, and 6.5% in Europe. Subsequently, in Europe the proportion of feminine founders is barely increased than within the U.S. however it isn’t one thing to brag about given how low the numbers are. Silver lining, presumably, North America has the best proportion of feminine govt crew members. Corporations in North America with at the very least one feminine founder have traditionally obtained the best median funding as nicely, given the energy of the enterprise capital business within the area. It isn’t all that doom and gloom.

Nonetheless, scaling can be a difficulty: alarmingly, solely 8 female-founded corporations have greater than 1,000 staff. That represents 5 corporations in Asia, two in Europe and only one in Latin America. Europe has 149 high fintechs and solely 12 feminine CEOs. That’s fairly dire.

Within the UK, a mere 17% of fintech corporations have feminine founders. In the meantime, girls account for lower than 30% of the sector’s total workforce, based on Innovate Finance. As well as, girls obtain simply 3% of enterprise capital funding within the sector. Once more, it signifies that startup traders are much less prepared to spend money on female-led fintech corporations.

There are some constructive developments…

The present state of girls in fintech is way from implausible. Nonetheless, there are constructive developments that make lots of people inside and out of doors the business assume that the state of affairs is enhancing. And that the longer term will probably be a lot brighter.

There was some constructive motion within the fintech business and the state of variety is slowly however certainly progressing. Right this moment, 13% of European fintechs have feminine founders which signifies that it’s higher than the general firm creation statistics. There are many high female-founded fintech startups which are taking the European market by storm: Starling Financial institution, Lovys, Azimo, Mambu, Billie, Molo, PensionBee, Pollinate, Fluidly, or GoHenry, to call a number of.

Though it’s making use of to a broader scope of corporations, France handed a regulation greater than 10 years in the past to impose gender parity in Boards of Administration and senior administration of medium to massive listed corporations. The French authorities can be serious about constructing on this regulation to push even additional into stronger variety governance. The EU adopted go well with not too long ago, asserting that in June 2022 that it’s concentrating on that at the very least 40% of the underrepresented gender should be represented in non-executive boards of listed corporations or 33% amongst all administrators. That’s constructing on the truth that Europe has many extremely certified girls with 60% of present college graduates being feminine.

There’s hope that Canada might comply with go well with as solely 17% girls are board members proper now. The UK can be stepping into the identical route.

This has a constructive influence on the administration composition of corporations in all sectors together with monetary providers. It forces corporations to construct a pipeline of future feminine leaders and to deeply overview the way in which persons are employed and promoted.

Going up!

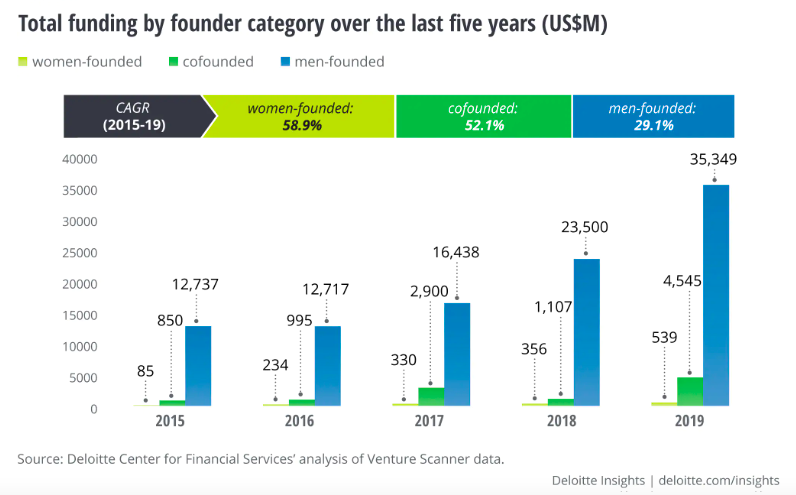

As of 2021, startups based by girls have considerably elevated their median valuation. It went from $30 million to $45 million within the final yr. Late-stage startups additionally went up 69% from $70 million to $120 million. The traits for enterprise capital funding involving women-led fintechs is anticipated to develop: lots of their companies skilled unimaginable resilience in the course of the international financial downturn.

Funding for women-founded startups grew at a compound annual development price of 59%, whereas funding for men-founded corporations grew by 29.1%. Ladies fintech leaders convey distinctive views to the fintech house, experiencing fintech merchandise differently than males. Corporations with the best variety of girls in high administration had a 41% increased return on fairness than the common.

For example, Canada’s Ladies Entrepreneurship Technique has positioned the nation as a pacesetter in the case of supporting the launch of female-led companies, with a purpose of doubling the variety of feminine entrepreneurs by 2025.

Federal and provincial governments, in addition to personal funders, have launched a number of insurance policies and applications centred round serving to girls finance, develop and scale their companies. Monetary establishments need to bolster gender variety initiatives. Many corporations have now integrated gender variety efforts into their funding methods.

For example, the launch of Goldman Sachs’s GS initiative which goals to take a position $500 million in gender-diverse corporations and funding managers. Likewise, JP Morgan, in partnership with The Vinetta Challenge, not too long ago launched an initiative to help girls founders by offering them larger entry to capital, networking alternatives, and advisory providers.

The gloom view

There’s additionally a view that the longer term is reasonably gloomy. With this extra compliance burden on European fintechs to work on their variety so as to do an IPO and turn into a listed firm, there’s the cynical view that these corporations might look to the U.S. or Asia and their much less stringent frameworks so as to keep away from doing the arduous work. Or keep personal for longer so as to by some means keep away from scrutiny.

European fintechs are already trying to North America to go public, citing a deeper pool of traders as the primary cause. Now, cherry on the fintech cake, it can be a strategy to preserve the established order by avoiding the governance and quotas imposed in Europe to get to a greater variety on the high of many organisations. That isn’t significantly far-fetched. It isn’t arduous to think about a column within the slide of a Board presentation itemizing “much less stringent governance necessities” as a pleasant strategy to justify why a fintech firm ought to go public outdoors of the EU.

What else could be carried out?

Given this gloom view of the world, it’s fairly sure that rather a lot could be carried out. However what, precisely? Relying on the stakeholders, a number of issues must occur.

Fintechs

With the intention to be sure that they embrace feminine clients, fintechs should collect knowledge on the gender make-up of their buyer base. That’s essential: monetary merchandise made by males for males are inclined to have a pure bias and miss some necessary specifics. Among the many 45 fintechs within the Inclusive Fintech 50 Benchmarks report, solely 20 might report plenty of feminine clients, indicating a knowledge hole. This knowledge will allow fintechs to trace their contribution to feminine monetary inclusion and determine areas for development.

Ladies founders

Contemplate different sources of capital: Ladies are at an obvious drawback in the case of conventional fundraising. However crowdfunding generally is a very helpful supply of preliminary capital. Particularly throughout instances like this, when securing conventional funding could also be more and more difficult.

Ladies must be extremely seen to traders and community between one another. Trade associations and organisations can play a useful position with this, each in underscoring the mandate for larger variety in funding capital.

Traders

Suppliers of capital have an enormous position to play. For example by enhancing networking entry and welcoming girls to enterprise capital corporations. It’s essential to unfold crucial funding help to early-stage fintech entrepreneurs of all kinds, not solely led by males.

Traders must widen the funding lens & actively keep away from unconscious gender bias within the VC pitching course of. A 2014 research by Harvard Enterprise Overview concluded that traders usually make funding choices based mostly on gender. Moreover, the research revealed that after listening to equivalent pitches given by women and men entrepreneurs, traders most popular pitches made by males.

One other research discovered that enterprise capitalists usually posed completely different inquiries to women and men entrepreneurs. Males had been extra more likely to be requested in regards to the potential for positive aspects, whereas questions towards girls targeted extra on the potential for losses. Apparently, this occurred whether or not the traders had been males or girls.

Researchers

Analysis organisations can present useful proof to construct a case for funding in female-led fintechs and the nuanced limitations that female-led fintechs face. Analysis is a powerful weapon so as to foyer governments and regulators. It forces public our bodies to behave and do one thing about gender imbalance and lack of variety in corporations. Constructing upon work by organisations reminiscent of Ladies’s World Banking, researchers can exhibit that female-led fintechs produce robust monetary returns whereas additionally making distinctive contributions to monetary inclusion.

Further analysis is required to look at the challenges confronted by feminine fintech founders.

Additional analysis ought to look at the position of fintechs in serving girls. Some inquiries to discover additional can embrace:

- the way to monitor the efficiency of fintechs;

- the way to co-create merchandise and options with feminine clients;

- efficient advertising methods to onboard girls;

- the connection between fintech and the SME credit score hole;

- and whether or not credit score scoring algorithms introduce gender bias

The world as a complete

Increasing visibility for feminine employees within the business has the potential to unfold consciousness of their success tales and encourage rising feminine entrepreneurs to take an opportunity and get into the sphere.

Function fashions can play an enormous position in driving constructive change by inspiring different girls to comply with of their footsteps. For example, success tales just like the certainly one of Dhivya Suryadevara within the U.S. has the potential to encourage hundreds of girls throughout the nation but in addition globally.

Corporations must implement family-friendly insurance policies. Work-life stability is just not a gender problem however impacts disproportionally girls when work environments are inflexible. The obligations of family life goes throughout genders. An “agile” working atmosphere needs to be the purpose of each organisation; one which flexes to help the wants and realities of staff within the digital age.

{kind=link}